API First Quarter Summary 2020

LOCAL MARKETS IN A NUTSHELL

Local equity markets had a very poor performance in the first quarter of 2020, in response to the Coronavirus pandemic. The JSE All Share Total Return Index fell by 21.4% over the quarter.

Chart: Performance of the FTSE/JSE All Share Index over the past ten years (2009/01/01 – 2020/03/31)

Source: Trading economics

The outlook at the start of 2020 was of optimism, particularly for South African stocks which were already trading at depressed prices.

There is a valid concern about a global recession over the year ahead, which has been priced into the local stock market.

In previous quarterly summaries, we noted that markets were expected to continue to remain volatile going forward. Due to what is being referred to as a “Black Swan” event i.e. the Coronavirus pandemic, market volatility has been much higher than investment managers and economists expected.

“Volatility is here to stay for some time, or at least until Covid-19 cases stabilise“.

Nazmeera Moola – Head of SA Investments at Ninety-One, formally Investec Asset Management

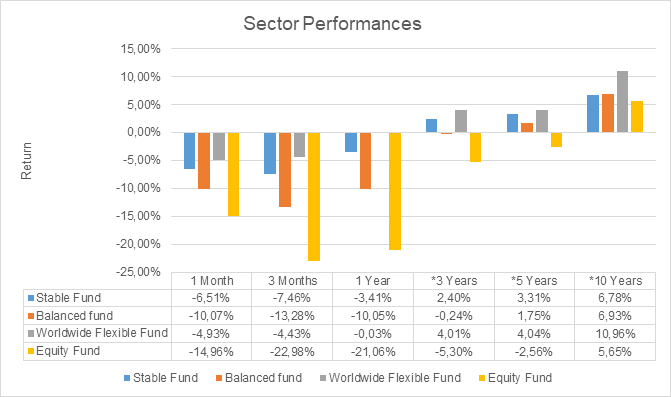

Source: Money Mate 31/03/2020

* Annualised Performance

WE HAVE BEEN HERE BEFORE – MARKETS CRASH

Since 1976 the local stock market has endured six market crashes as shown below. We are currently experiencing the seventh market crash. As the title suggests we have been here before and we will be here again in the future.

Data as of 25-03-2020

The difference in this market crash is that South Africa has been in a technical economic recession on various occasions in recent years with accompanying poor returns in our stock market. The JSE All Share Index was last at these levels in 2012. Fund managers look at the low share prices with optimism for great returns going forward. However, investors have experienced the last 5 years of poor performance as disappointment.

Understandably therefore, they are feeling the current market crash particularly acutely with their tolerance for poor returns already having been stretched.

The chart below represents the performance of the JSE All Share Index (blue line) against its long-term average trend line (grey line). Since 1996 the JSE All Share Index has trended upwards as one would expect from the equity market over a long period of time.

The ‘Corona crash’ has resulted in the index falling well below the long-term trend line. This gives investors some perspective as to why fund managers are expressing optimism over the valuation of the local stock market at these levels. The market is at an exceptionally cheap point relative to it’s history.

JSE All Share Index Trend Line

Source: Trading Economics 1996/01/01 – 2020/03/31

When the market initially crashed in reaction to the news of the Coronavirus pandemic, there was a sense that it had overreacted. Since the market bottomed on the 19th of March, it had recovered by 15.60% by the 31st of March. At the time of writing, the market is now up 27.93% since it bottomed. In order for investors to participate in the recovery, they needed to remain invested.

“The temptation to give in to one’s emotions is enormous. But to do so would be a big mistake. Investing is always an exercise in conquering one’s emotions. In times of bad news, asset prices will almost always be low. The primary objective of investing is to own more when prices are low and to own less when prices are high. As tempting as it is to ‘go to cash’, we do not believe that this is the right answer.”

Karl Leinberger, CIO, and John Parathyras, Global Developed Markets Analyst, Coronation Asset Management

MOODY’S DOWNGRADE – WHAT NOW?

The much-awaited downgrade as finally taken place. Arguably, it has however come at a bad time, in the midst of a global pandemic and during a nation-wide lock down which will see government debt rise beyond already unsustainable levels.

A downgrade is bad for South Africa as we will have to pay a higher premium to borrow money i.e. we will have to offer higher interest payments to lenders. Additional government borrowing is needed to sustain our expenditure in the short to medium term.

The downgrade has already been priced in for some time now. Until now, the question has generally been “when will the downgrade take place” rather than “will a downgrade eventually happen”. The uncertainty of a looming downgrade has potentially had a negative impact on our market due to the poor sentiment around our near junk rating.

The downgrade has caused our local bonds to become very attractively priced with SA bond funds falling 9-10% in March. As a result, many managers have been buying into them as they have sold off.

Despite the long-term economic consequences of being downgraded to sub-investment grade, now that the penny has dropped the uncertainty has been removed and the market can start to adapt.

It is also important to note that being a sub-investment grade country in terms of our credit rating, doesn’t necessarily mean that our economy is doomed and that international businesses won’t want to participate in our local economy.

“A sub-investment grade credit rating doesn’t mean that it’s the end of the economy, and that we can’t do business.”

“There are many sub-investment grade economies that are doing quite well. In fact, as an example, history shows that countries such as Brazil didn’t collapse after being downgraded to sub investment grade and in many ways started to perform better given that investors had greater certainty.”

Maarten Ackerman, chief economist and advisory partner at Citadel.

FORWARD OUTLOOK (LOCAL)

The forward outlook for the local economy over the next 12 months is worrisome as the world faces a potential global recession, while South Africa probably faces an extended recession. The South African Reserve Bank has slashed its growth forecasts for this year, predicting that the economy could shrink by between 2% and 4%.

Stock market performance over any one year, however, does not necessarily reflect the performance of the economy.

There are still many unknowns around the CV19 infection rate in many countries such as South Africa. Should we be unable to ‘flatten the curve’ within the next 2-3 months our situation may worsen, leading to more drastic steps to curb the spread. South Africa was one of the countries fortunate enough to implement a lock down before the crisis grew too large to manage. In the coming months this may prove to have been a very important decision.

The local market could see some form of a short-term recovery which is supported by government interventions such as lowering interest rates and implementing effective stimulus plans which can create positive sentiment, which in turn could drive the market. We might however also see the reverse effect, where with markets falling to new lows due to a global sell off in ‘risk’ assets.

The likely end to the global pandemic is the creation of a vaccine which experts feel will take at least 12 months to develop. A vaccine appears to be the biggest hope for renewed economic growth for the local economy.

“Our base case is that it will end with a vaccine +12 months hence, although we hope that an existing remedy will be effective before that.”

“As tragic as the Covid epidemic is, we will come out the other side. And when that happens, most economies will benefit from pent up demand, unprecedented fiscal and monetary stimulus, and record-low oil prices. Markets are likely to rally when we all least expect it. Will it be a medical breakthrough (which could happen at any time)? Will it be the point of peak infections? Will it be the lifting of lockdown? Who knows?”

Karl Leinberger, CIO, and John Parathyras, Global Developed Markets Analyst

Coronation Asset Management

OFFSHORE MARKETS IN A NUTSHELL

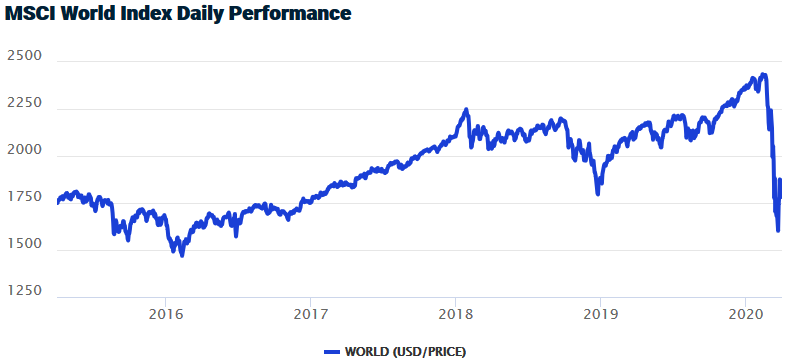

Global markets have undergone a market crash with the MSCI World Index falling -21.44% in USD over the first quarter of 2020. As the Coronavirus has spread around the world, markets have increasingly priced in the possibility of a global recession. This was accompanied by a crash in the oil price, initially due to a disagreement between Saudi Arabia and Russia and exacerbated further by falling demand due to the global CV19 pandemic.

The graph below represents the World Equity Index over 5 years in dollar terms.

*Performance as of 31/03/2020

For the first time in several years, the quarter saw concerning signs in global growth statistics, particularly in the US market. The US has seen a surge in the number of people who are applying for unemployment grants. Although unemployment in the US has previously been at historic lows, the concerning factor is how quickly the unemployment numbers are growing.

The US also seems to have taken a less definitive stance on prevention methods required to flatten the curve. Many countries around the world have implemented a “national lock down” as a radical step to control the virus.

Although the US president has expressed that he doesn’t anticipate a national lock down, they may be forced to implement one as the number of deaths begin to rise.

In the meantime, interest rates in the US have fallen to almost 0% in an effort to the prop up economy. The US has also agreed to a stimulus package with further measures expected to be deployed in the coming months.

THE RECESSION TO COME?

Many investors are asking the question as to how the global virus is affecting their portfolio and perhaps considering de-risking their portfolio “to prevent further losses”?

To address the question with substance beyond “take a long-term perspective” we have to consider what the experts are saying.

The world is now in a global meltdown. Some are calling this an artificial recession as its due to the constriction of economic activity due to national lock downs and social distancing measures that have been implemented around the world to differing extents. This differs somewhat from “traditional recessions”.

What are the experts saying?

Schroders

Keith Wade, Chief Economist & Strategist at Schroders suggests that we are likely to see a recession in the first half of 2020 as economic activity contracts due to people being unable to go to work. Unlike the Global Financial Crisis, Keith Wade believes that a rapid comeback is possible under the right conditions. As people are able to go back to work and economic activity increases, we could see a recovery in both the economy and the markets.

T. Rowe Price

Alan Levenson, Chief US Economist at T. Rowe Price suggests that markets may continue to fall, however when people are able to return to work the market should accelerate. A sentiment best expressed by the heading of an article which was authored by Alan, “Recession 2020 – Deep but Short”

Julius Baer Research Group

In a recent report titled “COVID-19 UPDATED SCENARIO ANALYSIS” the group noted the points:

- Equity market volatility is at historic highs. In fact, greater than that of the Global Financial Crisis according to the VIX Index.

- Goldmans Sachs risk appetite indicator suggests that the markets are in extremely bearish territory, greater than that of the Global Financial Crisis.

- The next 6 months will see a global recession.

- We should see a recovery in the second half of 2020.

BCA Research Group

In their recent report, BCA Research Group have also noted the following:

- US stocks may have further to fall.

- We are likely to see a recession over the next 6 months.

- A US reaction to effectively flatten the curve is crucial for a sustained economic recovery.

There is enough consensus by various managers and research houses to suggest the following views:

Positive views

- Valuations are cheap and therefore many managers are in fact buying into the market rather than selling out.

- Due to the artificial nature of the recession, we could see a relatively quick recovery in both the global markets and global economies by the end of the year, should people be able to return to work.

- Central banks and governments around the world are helping to stimulate the various economies.

- A market recovery is likely to be strong, coming off such a low base.

- Countries such as China, South Korea, Switzerland, Netherlands and Australia have appeared to have flattened the curve.

Negative views

- Markets have the potential to continue to fall.

- Some sectors of the economy will see capital destruction and a slow recovery.

- Debt levels around the world will continue to rise.

- If the US is unable to implement effective prevention measures, they may be unsuccessful in flattening the curve by the middle of the year. This could have drastic consequences for the US economy.

- National lock downs may be extended which will further negatively impact the global economy.

What does this all mean?

Unlike previous global recessions, we could see a relatively quick recovery within the next 12 months. It took 3 years for markets to recover from the Global Financial Crisis.

Within the next 12 months, we may continue to see markets fall as new data becomes available which means that markets are likely to remain volatile for the rest of 2020.

The light at the end of the tunnel is a possible vaccine which would see the threat of the virus being eliminated. In the short-term our hopes rests on flattening the curve, whilst allowing economic activity to continue.

The next 3 – 6 months will be vital to see if the current views of “experts” prove accurate or whether a longer recession is more likely.

What does this mean for your portfolio?

With the recognition of an uncertain outlook going forward it’s important for us to acknowledge that the fund managers within one’s portfolio are in the best position to navigate these unprecedented times.

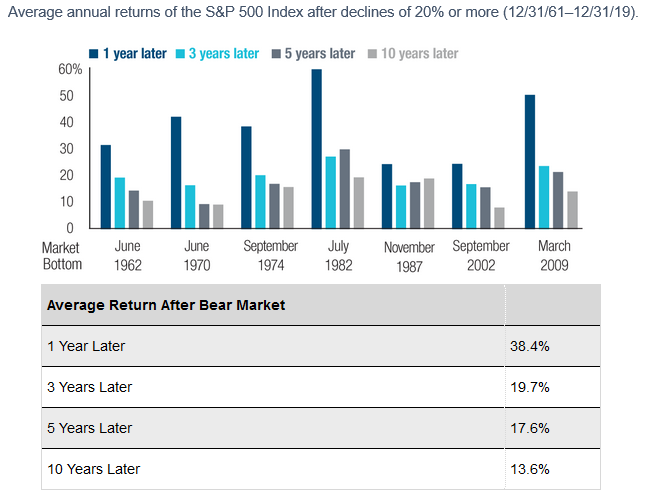

The chart below is a sober reminder of how markets recover from crashes and in order to benefit you must remain invested.

The dark blue bar represents the 1-year return once the S&P 500 Index has bottomed, following a fall of 20% or more.

Source: T. Rowe Price

FORWARD OUTLOOK (OFFSHORE)

The forward outlook for offshore assets appears to be dependent on the extent to which countries are able to control the spread of the Coronavirus. The consensus amongst asset managers and economists is that we should see a recovery over the next 6 – 12 months. Although this is by no means a guarantee the outlook does appear to be positive over the next 12 months. The fact that the current crisis is due to an existential event has caused policy makers to implement controls which have resulted in the recessionary environment. These controls, namely national lock downs, are expected to be lifted as soon as it is safe to do so – after we see a flattening of the curve.

There is likely to be consistent volatility going forward, however there is more optimism around the upside than there is on caution or fear around further downside.

An investor without investment objectives is like a traveler without a destination. During times of uncertainty our investment objectives are what ground us in our investment decisions.

As mentioned in the quote below, the “pain” that investors are feeling will be followed by a gradual healing in the global financial markets over the period to come. Whether it takes 6, 12 or 18 months for a global recovery, decisions that are made in the short term based on fear or greed and not sound financial planning principles, could lead to poor long-term outcomes.

“We expect the global economy and financial markets to transition from intense near-term pain to gradual healing over the next six to 12 months. However, there is the risk if not the likelihood of an uneven recovery, with significant setbacks along the way and some permanent damage that is not recouped.”

Joachim Fels, Global Economic Adviser and Andrew Balls Chief Investment Officer Global Fixed Income. PIMCO